To understand if you can fall victim to tax foreclosure you first have to determine whether you have an escrow account. Government-backed loans require an escrow account. Lenders of conventional loans that are not backed by the government can decide if they want to have an escrow account or not. Once you have an escrow account, you don't need to worry about paying property taxes because your loan servicer takes care of it. If you are a homeowner who does not have an escrow account for your mortgage or you have made all of your mortgage payments and own your home completely, you could be served with tax lien foreclosure documents. Tax lien foreclosure is a foreclosure that takes place after you fail to pay your property taxes. The foreclosure is initiated by the county that you live in because they have the lien on your home once you fail to pay the tax.

When you pay a mortgage on your home every month, it can sometimes seem like there are so many entities involved in the transaction. One entity you consistently keep hearing from is your mortgage servicer. What exactly does your mortgage servicer do?

If you are fortunate enough to be granted a loan modification, it is such a relief to know that you have saved your home! Almost losing your home to a foreclosure can be a scary wake up call that you hope to never have to go through again. Some people unfortunately do face foreclosure more than once, and when this happens there are many things to consider. One of them is whether you can modify your loan again.

Finding an attorney to assist you with your foreclosure can be a daunting and expensive task. It's important to be aware of all of your options when you are challenged with a notice of foreclosure.

You can proceed pro se, but a better alternative is to seek free legal help. Many states have free legal aid services in every county that will find an attorney to work on your foreclosure case for free. Your eligibility for these services depends on various factors such as: residency, type of residence being foreclosed on, and your family or individual income. Depending on your case, legal aid services can offer any kind of help, from the filling out of court forms all the way to representing your case in court.

A loan modification can allow you to keep your home and avoid foreclosure after falling behind on your mortgage, but it's not necessarily all roses. In fact, there are some downsides to loan mods that your lender may not go out of their way tell you about.

If you don't know, a loan modification is a permanent change to one or more of the terms of your mortgage, such as the term, interest rate, and monthly payment.

A loan modification is often the only hope many homeowners have to keep their home following a default. They can be great, however if you need one, you should be aware of the following:

When you are served with foreclosure documents it can be devastating. Given the current situation, you are faced with the possibility of losing your home during, what appears to be, a never-ending COVID-19 pandemic.

This foreclosure also didn't take place because you have tons of disposable income laying around. So now you have to decide how you are going to save your home. The idea of hiring an attorney in the wake of being served with foreclosure documents seems impossible: if you didn't even have enough money to pay your mortgage, how can you think about hiring a lawyer? So now you're considering representing yourself in court to save your house and to save the attorneys' fees.

Amerihope Alliance Legal Services, which focuses on providing foreclosure defense and loan modification assistance, is proud to have accepted numerous awards for providing excellent service to our clients over the last 12 years.

Here are just a few of the things I overheard last week:

- "Wells Fargo gave me a 3 month forbearance, I don't need to make any payments."

- "If they can't foreclose, why should I make my mortgage payments?"

- "Mr. Cooper is letting me skip three mortgage payments, I ordered new patio furniture."

How would you respond to each of these? Let's take a look.

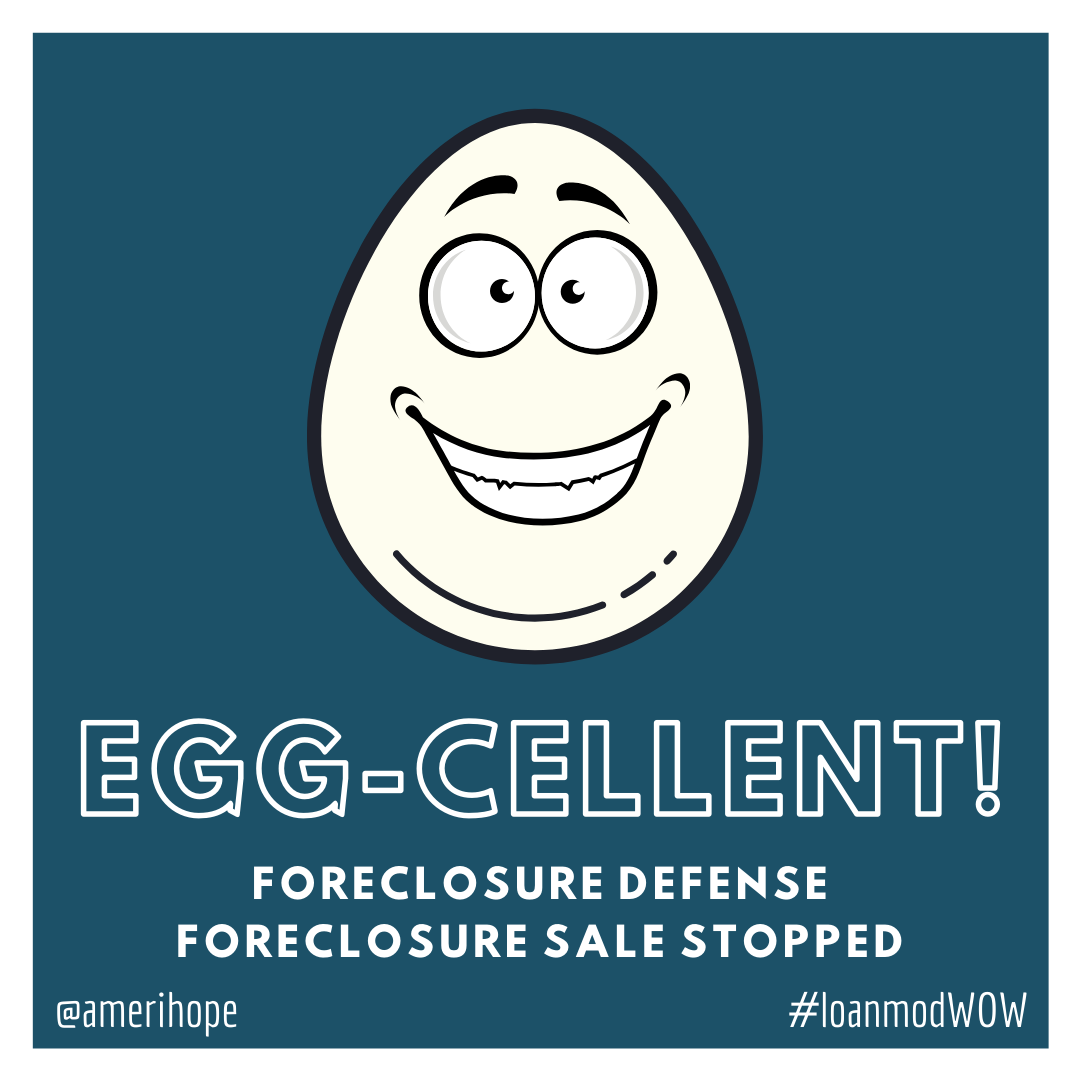

Mr. Cooper Loan Modification

We received a modification for our client's mortgage with Mr. Cooper. They were 10 months behind, and in an active foreclosure case. This new modification lowers their mortgage payments from $803.82 per month to $743.64.

Do you have a Mr. Cooper mortgage that's past due? See some of our other Mr. Cooper case results here.

Only if you have to.

Our attorneys' COVID-19 advice:

- If you can afford to keep paying your mortgage during a hardship caused by Coronavirus, keep paying your mortgage.

- If you cannot afford to make your mortgage payments, our lawyers want to do everything possible to help you understand your options and be protected from your bank's misrepresentations.

Q: Why?

A: Because in our experience, most mortgage "disaster relief" becomes a nightmare.