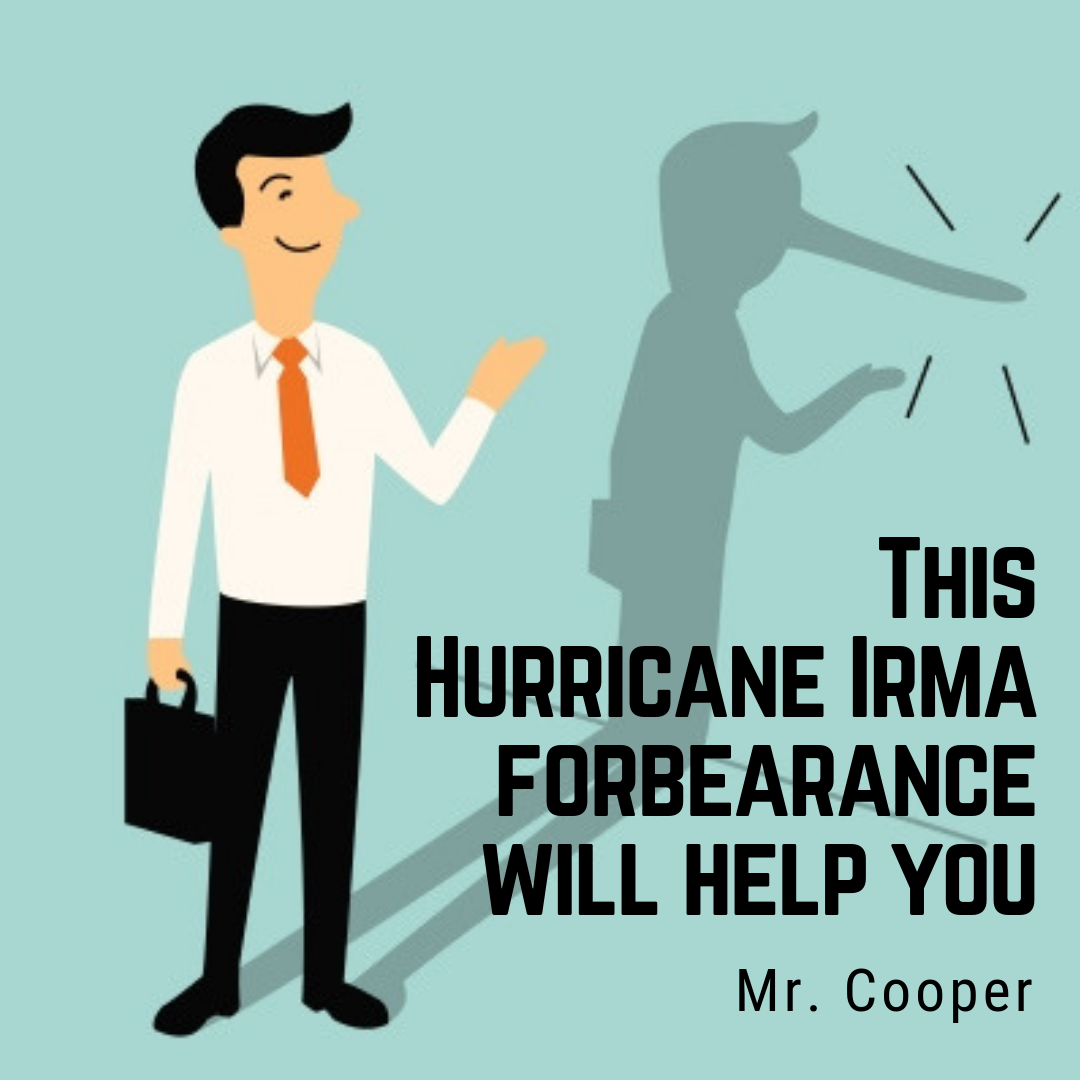

Only if you have to.

Our attorneys' COVID-19 advice:

- If you can afford to keep paying your mortgage during a hardship caused by Coronavirus, keep paying your mortgage.

- If you cannot afford to make your mortgage payments, our lawyers want to do everything possible to help you understand your options and be protected from your bank's misrepresentations.

Q: Why?

A: Because in our experience, most mortgage "disaster relief" becomes a nightmare.