Disclaimer: These results should not be taken as a guarantee, as each case is unique. We have helped over 7,000 homeowners. Here are a few of their stories.

Recent Posts

Homeowners in New Jersey have a right to adjourn a sheriff's sale of their home for 14 days for any or no reason by paying a small fee.

And this can be done twice.

This foreclosure avoidance tool is called a statutory right to adjourn sheriff's sale. (Adjournment means a temporary postponement of a court action.)

It's not a permanent way out of foreclosure, and it doesn't cancel the sale, but it's a great tool for homeowners to use to temporarily stop the sale of their home when no other option is available.

Disclaimer: These results should not be taken as a guarantee, as each case is unique. We have helped over 7,000 homeowners. Here are a few of their stories.

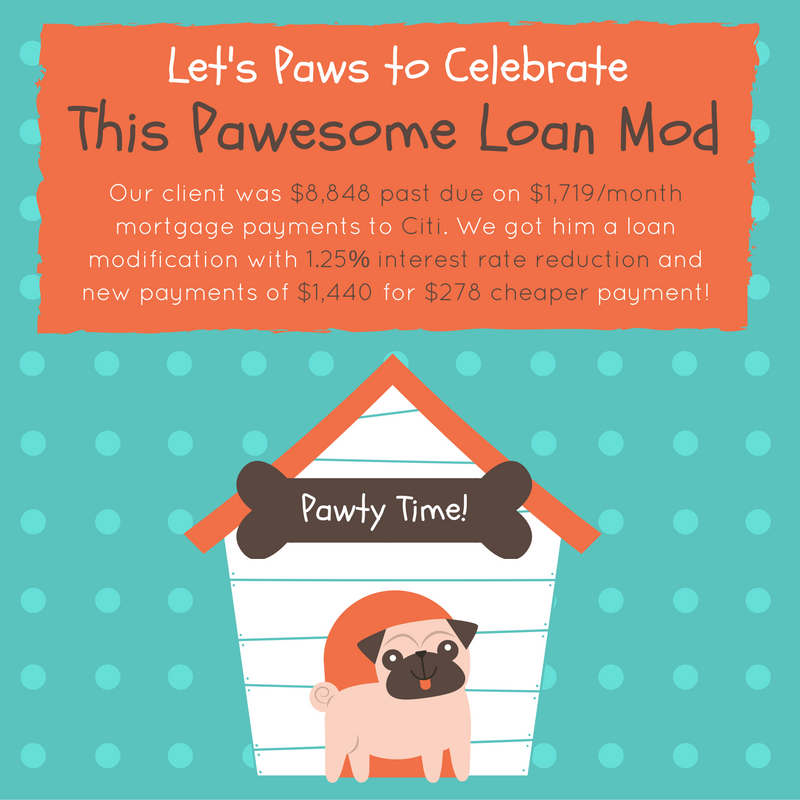

Every week we obtain loan modifications for our clients with a variety of loan servicers. You can see these results as they are announced on Twitter (#loanmodwow) or Facebook. Here are some of our results from this week with Rushmore, Citi, SLS, and Caliber:

Rushmore

Fresh start! Our Rushmore client has a 3 month in-house trial loan modification plan after falling 10 months and $22,532 behind on mortgage payments.

Disclaimer: These results should not be taken as a guarantee, as each case is unique. We have helped over 7,000 homeowners. Here is one of their stories.

Karen Reyes had a problem with the mortgage on her Florida home. (That's not her real name, but a pseudonym to protect our client's real identity.) Mrs. Reyes had fallen behind on her mortgage payments after the death of her husband and the bank wanted to foreclose.

If you have a mortgage with Chase and are having difficulty making your monthly payments, or have already defaulted, a loan modification may be right for you.

A loan modification can bring your monthly payment down to an affordable portion of your income, help you avoid foreclosure, and return your loan to normal servicing.

Unless you have the cash to reinstate your mortgage after falling behind, a modifying your loan is probably the only solution that allows you to keep your home.

A loan modification involves making a permanent change to one or more of the terms of a loan. The interest rate on a loan can be lowered, the term length extended, and principal can be forgiven or restructured to bring the payment down. Unlike a refinance, which can also bring a mortgage payment down, there are no closing costs associated with getting a loan modification.

Every week we obtain loan modifications for our clients with a variety of loan servicers. You can see these results as they are announced on Twitter (#loanmodwow) or Facebook. Here are some of our results from this week, which include results from Chase, Statebridge, Ditech, and SLS:

Central Mortgage

Trial modification payments drop by more than a third, from $1,524 to $972.00, for our client 13 months past due with Central Mortgage.

Let's say you fell behind on your mortgage, but haven't lost your home to foreclosure yet, and one day you come home to find that the bank has changed the locks on your doors and you can't get inside your home. How could this be? Are they allowed to do that?

If you're still living in your house, no, your bank isn't allowed to change the locks on your house. Even if you fell behind on your mortgage payments or are in foreclosure.

You're allowed to live in your home during the entire foreclosure process. If you're still living in the house after the home is sold in a foreclosure sale, the bank has to evict you before they can change the locks and take over the property.

But there is one exception that allows the bank to change the locks on your property even if you still legally own your home: when the property is abandoned and sitting vacant. Then it doesn't matter if foreclosure isn't complete yet or not.

From the point of view of the IRS, any of your debt that is forgiven is considered the same as income, and taxes must be paid on it as such. Forgiven debt has been called phantom income because it's not really income that's there. Despite that, it's still subject to taxation just like it was money you earned at your job.

But in 2007 the Mortgage Forgiveness Debt Relief Act became law, which exempts homeowners from having to pay taxes on forgiven mortgage debt. On January 1, 2017 the act will expire. When it does, forgiven mortgage debt will be taxable again.

Why the Mortgage Forgiveness Debt Relief Act Was Needed

The country has been experiencing a foreclosure crisis over the last decade. More than seven million homeowners have experienced foreclosure since the housing crisis began. As a result so many people had mortgage debt forgiven that the government stepped in to help them avoid even more financial damage with the Mortgage Forgiveness Debt Relief Act.

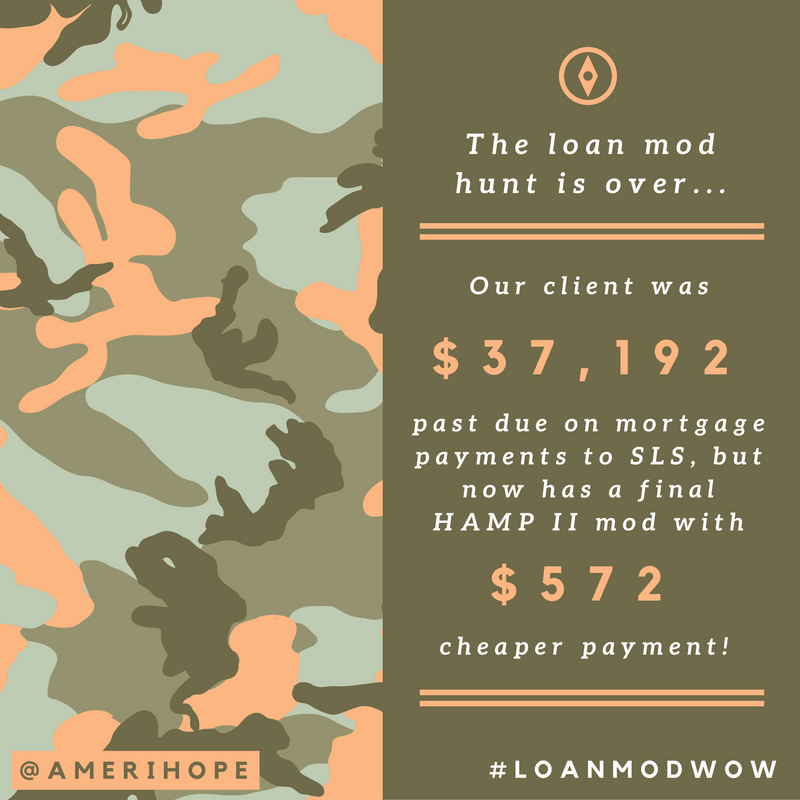

Every week we obtain loan modifications for our clients with a variety of loan servicers. You can see these results as they are announced on Twitter (#loanmodwow) or Facebook. Here are some of our results from this week, which include results from SLS, Citibank, Ditech, and Seterus:

SLS

20 months and $37,192 past due on mortgage payments to SLS, our client was approved for HAMP tier II loan modification with $572 in monthly savings!

Knock, knock. Who's there? A loan modification with $427 in monthly savings for our client who was 40 months behind with SLS, that's who.

The government's Home Affordable Modification Program (HAMP), is expiring at the end of 2016, and the mortgage industry has ideas about how to replace it.

HAMP, sometimes referred to as the Obama plan, became available to distressed homeowners in 2009 in response to the financial and foreclosure crises. Its goal has been to help delinquent borrowers keep their home with a more affordable monthly mortgage payment.

Now the Mortgage Bankers Association, a trade group representing the real estate finance industry, has released its own suggestions for how loan modifications should be implemented in a post-HAMP world in 2017 and beyond. It's called One Mod, short for One Modification.