If you put down less than 20% when you purchased a home, you probably pay for private mortgage insurance (PMI) every month. Private mortgage insurance protects the lender in case you can't make your payments and the house is foreclosed on. But what happens if you paid 20% down? Surely, that proves that your loan is not a risky one for the lender. I mean you have shown that you have a significant financial stake in the property. Pay attention, Mortgage Watchdog says that 70% of existing escrow accounts violate federal law by holding excessive balances. According to the Federal Deposit Insurance Corporation (The FDIC is an independent agency of the federal government responsible for insuring deposits.) Home loan errors are costing Americans $8 billion to $10 billion each and every year.

Attorney at Law, Gregory M. Nordt, Esq. has reached another milestone – 20 years of service and experience in the field. He has been practicing foreclosure defense, banking/finance law, tax law, and IRS tax controversy since 1995. Mr. Nordt, along with his team at Amerihope Alliance Legal Services, invoke candor, integrity, and expertise whilst defending their clients. All with the common end goal of achieving the best possible outcomes.

“I, along with our entire team, am extremely proud of our attorney Greg Nordt, that he has reached this career milestone with such integrity," said Amerihope Alliance Legal Services Operations Manager Sherrill Clark. "We applaud Greg for his long standing commitment and passion." All cases are unique and Mr. Nordt treats all clients with the respect and care they deserve. From the start, Mr. Nordt fights alongside his clients to ensure the end goal is met.

“There are so many talented people I work with. For the last three years our Managing

I’m attorney Nick Murado. I sue debt collectors and can fix your credit rating – for FREE!

If you have any debts in collections, you know the types of tactics the debt collector scum are willing to use:

- They have no problems insulting you, abusing you, or cursing you out.

- They love to call you at work, which can threaten the status of your employment.

- They cherish those early morning or late night calls, designed to disorient you and wear down your willpower, hoping you'd just pay them so they would go away and let you sleep.

- They relish those times they call your family, your neighbors, or your friends, attempting to convert them into tools of war to be used against you.

- They enjoy placing false, fraudulent, or otherwise incorrect information on your credit reports, tanking your credit rating.

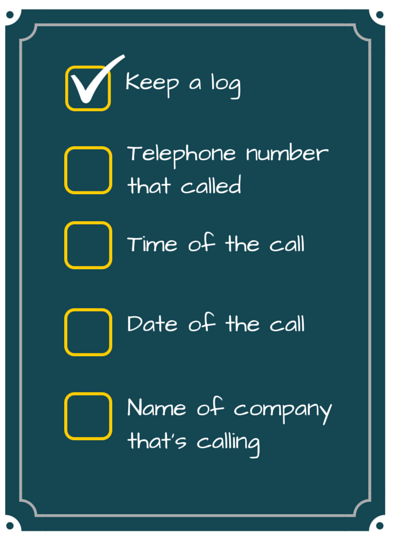

When a debt collector calls you, it's important to keep a record of what happened, especially if you think your rights may have been violated.

Consumer law attorneys need, at a minimum, the following information to begin a prosecution of your rights under the FDCPA, FCCPA, or TCPA:

- The number that called

- The time of the call

- The date of the call

- The name of the company calling, if known.

Any time a new number calls you, it is important to answer the phone at least once to make sure that a given phone number belongs to the same debt collection company. Once you have this information, you can hang up. Any future calls from that particular phone number can be logged as belonging to that same company.

1. Natural Disasters.

Floods, earthquakes, hurricanes, tornadoes, etc. During natural disaster, people will skedaddle from their homes and sometimes they never return.

2. War or Civil Conflict.

Violence, anarchy, etc. In times of war and civil conflict there are lots of people who will just abandon their homes and never ever come back.

When it comes to applying for a loan modification, your debt-to-income ratio is really very important. Having the right or wrong DTI ratio can make or break your loan modification. But what is debt to income ratio? Let's dive right in. President Obama's foreclosure prevention plan has it set up so that for your first mortgage, your Front-end debt-to-income ratio can be no more than 31 percent. This basically means that your house payment cannot exceed 31 percent of your gross monthly income. So if for example your monthly mortgage is $1,000, your gross monthly income should be at around $3,230 or more.

There are actually 2 debt-to-income (DTI) ratios to become familiar with:

- First there's your Front-end DTI ratio which is based on your house payment. Under the President's plan, the Front-end DTI ratio target of 31 percent only applies to your first mortgage. Other loans taken against your home such as a second mortgage or an equity line of credit are separate and are not a part of your Front-end DTI. Instead, you can calculate these other loans as a part of your Back-end DTI. But wait, what is Back-end DTI? I'm glad you asked!

- Besides Front-end DTI, you also have your Back-end DTI ratio which is based on all your monthly debt payments combined. This includes your house payment, credit card payments, auto loan payments.

If your loan modification was denied, don't worry: you're not alone. Loan modifications may be one of the hardest things to get approved without the assistance of an experienced attorney. After denial, your next step will depend on the reason why you were denied and where your home is in the foreclosure process.

As the second largest bank in the United States based on total assets, Bank of America has become a staple in nearly every home. More so, Bank of America has been an integral factor in the financing of millions of mortgages across the U.S. With such a considerable level of relevance in home mortgages, it's easy to assume that BOA is the shining symbol of excellence. However, Bank of America has consistently been amid a whirlwind of mortgage lawsuits and shady practices over the last few years.

Amerihope Alliance Legal Services managing attorney Gregory Nordt congratulates Florida Attorney General Pam Bondi who was re-elected to serve a second year term as Florida’s Chief Legal Officer. Attorney General Pam Bondi secured 55% of the vote with more than 5.6 million votes cast in the cabinet race.